Car insurance is a necessity for any driver—but that doesn’t mean you need to overpay for it. Many people assume that saving money on their premium means accepting less coverage or taking on more risk. But in reality, there are several smart, practical ways to reduce your car insurance costs without sacrificing protection.

If you’re looking to cut costs without cutting corners, here are some of the most effective ways to lower your car insurance rates while keeping your coverage solid.

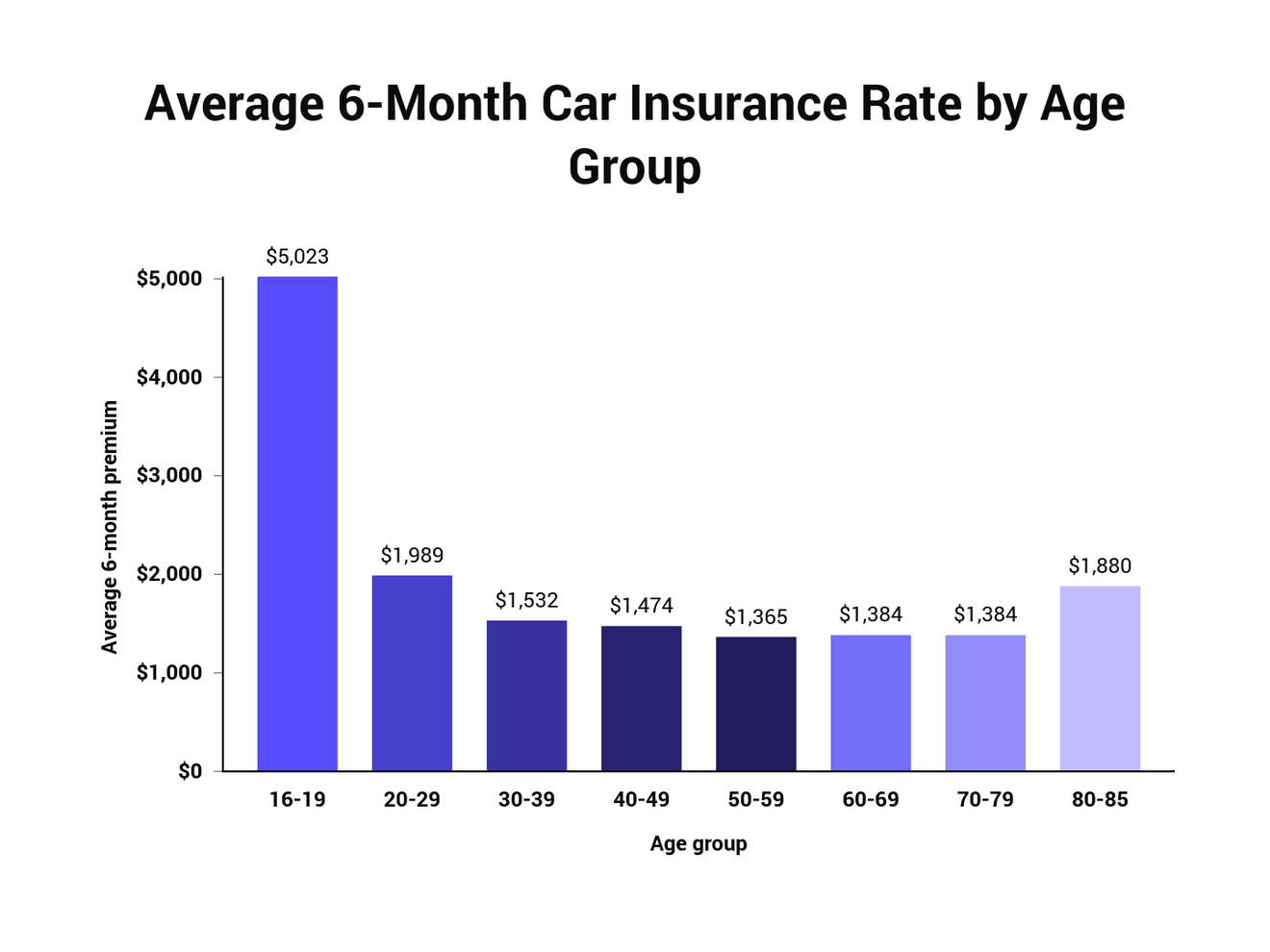

Maintain a Clean Driving Record

Your driving history is one of the biggest factors insurance companies use to determine your rate. The fewer accidents, speeding tickets, and violations you have, the better your premium. Safe drivers are rewarded with lower rates because they pose less risk to insurers. Even a single accident or ticket can raise your premium for years, so it’s worth taking the extra caution behind the wheel.

Bundle Your Policies

Insurance companies often offer significant discounts when you purchase multiple policies from them. For example, bundling your auto and home insurance (or renters’ insurance) with the same provider can lead to substantial savings. This not only helps reduce your premium but also simplifies your insurance management.

Increase Your Deductible

Raising your deductible—the amount you pay out of pocket before insurance kicks in—can lower your monthly premium. While this means paying more in the event of a claim, it’s a worthwhile strategy if you’re a safe driver and don’t anticipate frequent claims. Just make sure you have the deductible amount saved and accessible in case of an emergency.

Take Advantage of Available Discounts

Many drivers miss out on savings simply because they don’t ask. Insurance companies offer a wide range of discounts that may include:

- Good driver discounts

- Good student discounts

- Low mileage or usage-based insurance

- Vehicle safety feature discounts (anti-lock brakes, airbags, theft prevention systems)

- Membership or professional group discounts

It’s always worth asking your insurer what you qualify for.

Drive Less When Possible

If you work from home, use public transportation, or carpool, you’re likely putting fewer miles on your car than the average driver. Insurance companies often reward low-mileage drivers with reduced premiums, as lower usage means less risk of accidents. Some insurers also offer pay-per-mile policies that are ideal for infrequent drivers.

Consider Usage-Based Insurance Programs

Many insurance companies now offer telematics programs that monitor your driving habits through a mobile app or plug-in device. These programs track things like braking, acceleration, and time of day you drive. If you’re a careful driver, you could see substantial discounts. While some people may be wary of being tracked, it’s a great option for those confident in their driving behavior.

Review and Adjust Coverage as Your Car Ages

When your vehicle is new or financed, full coverage is often necessary. But as your car gets older and loses value, it might not make financial sense to pay for comprehensive and collision coverage. Reassessing your policy and removing or reducing certain coverage types can reduce your premium—just be sure you’re still adequately protected.

Improve Your Credit Score

In many states, insurers use your credit score as part of their risk assessment. A strong credit history can result in lower premiums because it’s often associated with responsible behavior, including safe driving and timely payments. If your credit score has improved recently, notify your insurer—your improved financial standing could earn you a lower rate.

Shop Around and Compare Quotes

One of the most effective ways to ensure you’re getting the best deal is by comparing quotes from multiple insurers. Prices and coverage can vary widely between companies, even for similar policies. Don’t just renew automatically each year—take the time to shop around. It’s often the quickest way to find savings.

Work With an Independent Insurance Agent

Independent agents aren’t tied to one insurance company, so they can shop the market on your behalf. They understand the nuances of different policies and can help you find the right balance between affordability and coverage. Their experience can also help you identify discounts and avoid paying for coverage you don’t need.

Lowering your car insurance premium doesn’t have to mean cutting corners or increasing your risk. With a thoughtful approach, you can find meaningful savings while maintaining the protection you need. From maintaining a clean driving record to adjusting your coverage and exploring discounts, every step counts.

Staying proactive, reviewing your policy annually, and communicating openly with your insurer can keep you in control of your costs—without compromising peace of mind on the road.